Guides

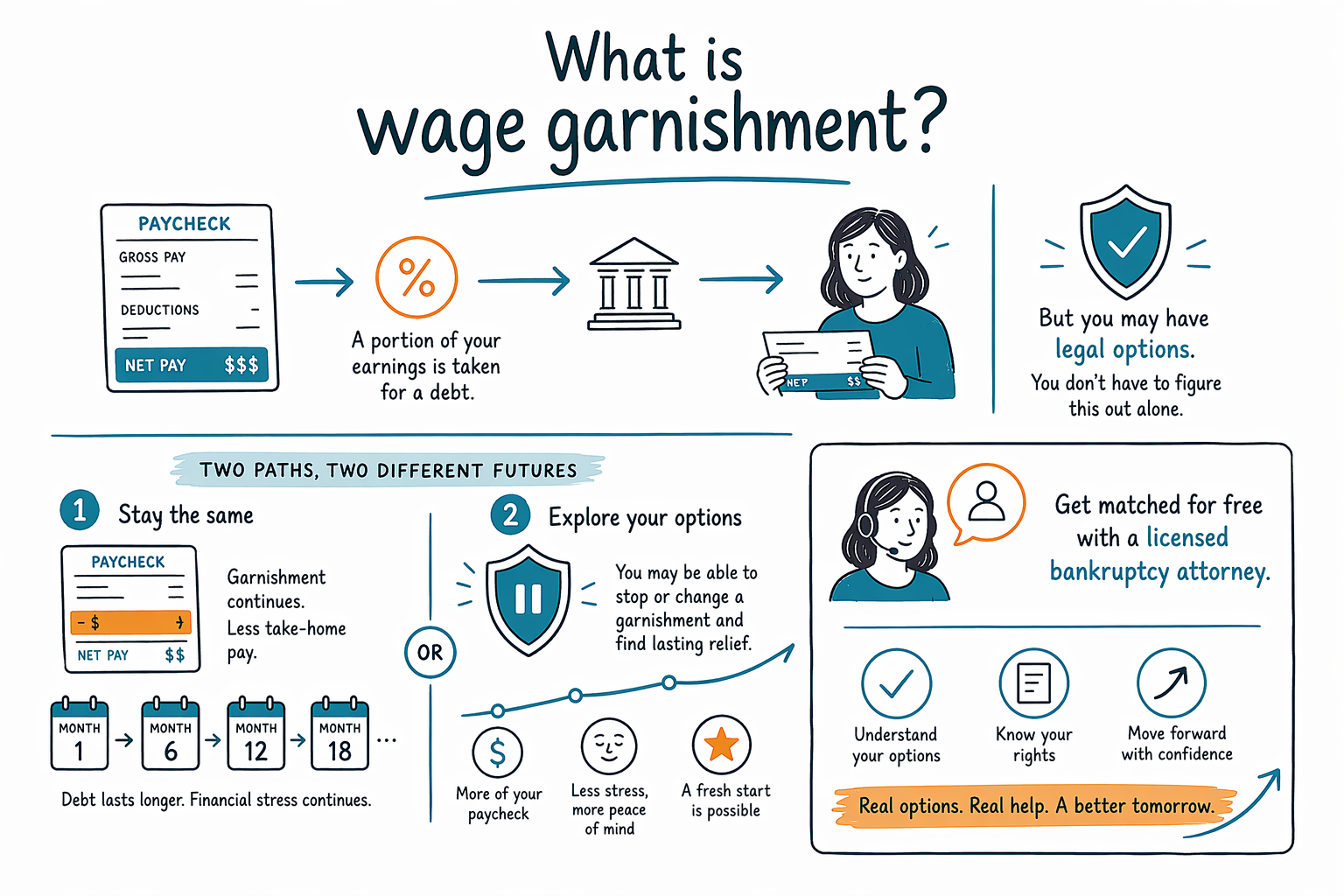

What is wage garnishment?

Wage garnishment means money is taken from your paycheck to pay a debt, usually after a court process. It can feel scary, but you may have options — including bankruptcy in some cases — and help is available.

What wage garnishment means

Wage garnishment is when part of your pay is withheld by your employer and sent to a creditor or another party you owe. In many cases, this happens after a creditor sues you, wins a judgment, and gets a court order. But some kinds of debt, such as child support, certain taxes, or federal student loan collection rules, may follow different procedures.

If your paycheck suddenly looks smaller, or your employer tells you they received legal papers, wage garnishment may be the reason. Many people first learn about it only after they are already behind on bills. You are not alone, and it does not mean you have done something morally wrong.

The exact rules vary by state and judicial district, and different debts follow different rules. This page is general educational information only, not legal advice. A licensed bankruptcy attorney in your area can tell you what applies to your situation.

How it usually happens

For many consumer debts like credit cards, personal loans, or some medical bills, a creditor usually must first sue you in court. If the creditor gets a judgment, it may then ask the court for permission to garnish wages. Your employer is then told to hold back part of your paycheck.

Not every debt follows the same path. Child support and alimony often have strong collection tools. Some tax debts and some government debts may be collected under different federal or state rules. Because of that, the notice you receive and the defenses you may have can be different.

A garnishment does not always last forever. It may stop when the debt is paid, when the court orders it stopped, when a settlement is reached, or when a bankruptcy case is filed and the automatic stay applies. Whether that stay will stop your particular garnishment depends on the type of debt and the timing, so it is important to speak with a licensed attorney quickly.

How much can be taken from a paycheck?

There are legal limits on wage garnishment, but the amount depends on the type of debt and the law that applies. For many ordinary consumer debts, federal law sets a cap, and some states protect more of your wages than federal law does. For child support, taxes, and certain other debts, the amount can be different.

That is why two people in different states can have very different results. State exemption laws, income level, the kind of debt, and whether you support dependents can matter. If you are already struggling to pay rent, food, transportation, or medicine, it is worth asking a local attorney whether too much is being taken or whether an exemption may apply.

You can learn more general background in our guides and overviews of chapters, but only a licensed bankruptcy attorney in your area can review the papers and tell you what protections may apply.

Can bankruptcy stop wage garnishment?

Sometimes, yes. When a bankruptcy case is filed, an automatic stay usually goes into effect right away. The automatic stay pauses most collection activity, including many garnishments, lawsuits, foreclosure actions, and collection calls. This is one reason people who are facing urgent collection pressure often speak with a bankruptcy attorney quickly.

But there are limits, and it is important to be honest about them. Bankruptcy does not erase every debt. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts caused by fraud. Also, whether a garnishment stops immediately can depend on the type of debt and the stage of the case.

For some people, Chapter 7 may be a better fit if they qualify and need a faster reset. For others, Chapter 13 may help them repay part of what they owe through a court-approved plan while catching up on secured debts like a mortgage or car loan. The right path depends on income, assets, debt type, and state-specific exemption rules. That is why a local legal review matters.

What to do if your wages are being garnished

If your wages are being taken now, try not to ignore the paperwork. Acting quickly can matter. Keep every notice from the court, sheriff, creditor, payroll department, or collection lawyer, and bring those papers to any attorney consultation.

Here are practical first steps:

- Ask your employer or payroll department for a copy of the garnishment notice if you do not already have it.

- Check what kind of debt it is: credit card, medical bill, child support, taxes, student loan, or something else.

- Gather basic documents such as recent pay stubs, court papers, and creditor letters.

- Do not send sensitive information like your Social Security number, bank account numbers, or credit card numbers through a matching form.

- Speak with a licensed bankruptcy attorney in your state as soon as possible if the garnishment is causing hardship.

If you are not sure where to start, CleanSlate Match can help you get matched with a licensed bankruptcy attorney near you. CleanSlate Match is a free matching service, not a law firm, not a lawyer, and does not file bankruptcy or create an attorney-client relationship.

What legal help may cost

Many consumer bankruptcy attorneys charge a flat fee for a Chapter 7 or Chapter 13 case, plus the court filing fee and a small required credit-counseling course fee. The real cost depends on the chapter you file, how complex your case is, and the district where you file. These are not quotes, just common ranges people may see.

For Chapter 7, attorney flat fees often range from about $1,000 to $2,500, plus a court filing fee that is commonly a few hundred dollars, and a modest credit-counseling fee. For Chapter 13, attorney flat fees are often higher — sometimes about $3,000 to $6,000 or more depending on the district and case complexity — plus the court filing fee and required course fees. In many Chapter 13 cases, part of the attorney fee may be paid through the repayment plan, but that depends on local practice and the attorney.

Cost can go up if there are lawsuits, business issues, many assets, disputed debts, tax questions, past bankruptcy filings, or urgent emergency filings. Always ask for a written fee agreement and confirm the attorney is licensed in your state. CleanSlate Match is free for the person seeking help. Participating attorneys pay a flat fee to take part in the service.

Wage garnishment means money is taken from your paycheck for a debt, but you may have legal options, and a free match to a licensed bankruptcy attorney can help you understand them.

Common questions

Can a creditor take my whole paycheck?

Usually no. There are legal limits, but the amount depends on the kind of debt and the law that applies. State and federal rules can be different, so a local attorney can tell you what limit applies in your case.

Will filing bankruptcy stop a wage garnishment right away?

Often it stops many garnishments because the automatic stay begins when a case is filed. But some debts are treated differently, and timing matters, so there is no guarantee without reviewing your specific case.

Can bankruptcy erase the debt behind the garnishment?

Sometimes, but not always. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud.

What information do I need to get matched with an attorney?

Usually just contact information and general intent: your name, phone number, optional email, state, a brief description of your situation, and your preferred language. You should not need to provide a Social Security number or bank or credit card numbers to get matched.

Is CleanSlate Match a law firm?

No. CleanSlate Match is a free matching service. It is not a law firm, not your lawyer, and does not create an attorney-client relationship or file bankruptcy papers for you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →