Guides

What happens if im sued for debt?

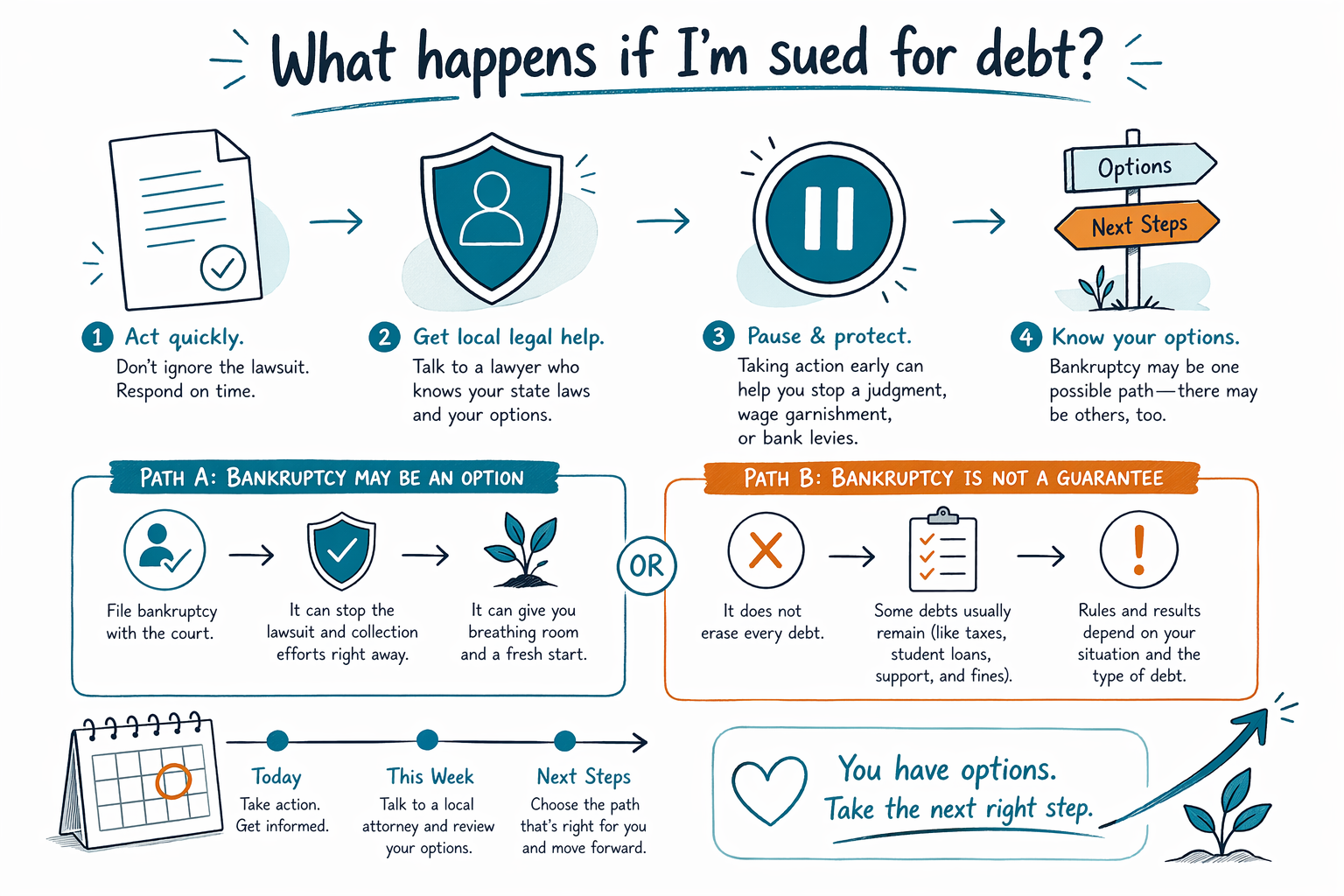

If you’re being sued for debt, it can feel urgent and scary — but you do have options. In many cases, you may be able to respond, protect important income or property, and get help from a licensed bankruptcy attorney near you.

First: do not ignore the lawsuit

A debt lawsuit is a court case from a creditor or debt buyer asking a judge to say you owe the money. If you do nothing, the court may enter a default judgment against you, which can make collection harder to stop.

That does not mean you have no choices. You may still be able to answer the case, ask for more time, dispute mistakes, or explore debt relief options. Rules and deadlines vary by state and court, so it is important to read every paper carefully and get local help soon.

If the papers mention a court date or deadline, treat that as serious. A licensed bankruptcy attorney in your area can tell you whether bankruptcy, a settlement, or another response makes sense for your situation.

What a debt lawsuit can lead to

If the creditor wins, the court may allow collection steps such as wage garnishment, bank levies, or liens in some situations. What can happen depends on your state law, the type of debt, and the court process.

If you are already dealing with wage garnishment, foreclosure, repossession, or repeated calls, this is a sign to get advice quickly. Bankruptcy may be one possible tool, but it is not the only one, and it is not the right fit for everyone.

The good news is that once a bankruptcy case is filed, the automatic stay usually pauses most collection activity right away, including many lawsuits, garnishments, and foreclosure steps. There are exceptions, and outcomes depend on the case.

How bankruptcy may help if you are being sued

Bankruptcy does not erase every debt, and it is not a promise that a lawsuit will disappear forever. But it can often stop the lawsuit while the case is active, and it may help remove some unsecured debts such as credit cards or medical bills, depending on the chapter and your facts.

Chapter 7 is often called a liquidation case. For people who qualify under the means test, it may discharge many unsecured debts, but some debts usually survive, including most student loans, recent income taxes, child support, alimony, many court fines, and debts from fraud.

Chapter 13 is a repayment plan. It can help people who have income but are behind on bills, especially if they need time to catch up on a home loan or stop a garnishment. Many people keep their home or car through exemptions or a Chapter 13 plan, but that depends on the state, your assets, and the court rules.

What to do right now

- Read the lawsuit papers and calendar every deadline.

- Save every letter, text, voicemail, and court notice.

- Do not share bank-account numbers, Social Security numbers, or other sensitive details with anyone unless you know who they are and why they need it.

- Gather basic contact information, a general description of the debt problem, your state, and your preferred language.

- Talk to a licensed bankruptcy attorney in your area and confirm the attorney’s bar license.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We can help connect you with a licensed bankruptcy attorney near you, but we do not file bankruptcy or give legal advice.

What bankruptcy typically costs

Most consumer bankruptcy attorneys charge a flat fee, plus the court’s filing fee and a small required credit-counseling fee. The total can change based on the chapter, how complex your case is, and the local district.

Very rough ranges for consumer cases are often something like:

- Chapter 7: attorney flat fees may be in the low thousands, plus the court filing fee and counseling fee

- Chapter 13: attorney flat fees are usually higher because the case is more involved, plus the court filing fee and counseling fee

Those are not quotes. Your actual cost depends on your case, your location, and the attorney. A local bankruptcy lawyer can explain the full cost up front.

How CleanSlate Match can help

We help people across the United States find a licensed bankruptcy attorney near them, in the language they are most comfortable using when possible. The service is free for you.

We collect only contact information and general intent — for example, your name, phone number, optional email, state, a general description of the problem, and your preferred language. We do not need your account numbers, income, or other financial details to start the match.

If you are feeling overwhelmed, you do not have to sort this out alone. A calm first conversation with a local attorney can help you understand whether bankruptcy, a settlement, or another path fits your situation.

If you are being sued for debt, act quickly, get local legal help, and know that bankruptcy may be one possible path — but it is not a guarantee and it does not erase every debt.

Common questions

What happens if I ignore a debt lawsuit?

The court may enter a default judgment if you do not respond in time, which can make collection easier for the creditor. Deadlines vary by state and court, so read the papers right away and get local legal help.

Can bankruptcy stop the lawsuit?

Often, yes. When a bankruptcy case is filed, the automatic stay usually pauses most collection activity, including many lawsuits. There are exceptions, so a licensed attorney should review your situation.

Will bankruptcy erase all my debt?

No. Bankruptcy can help with many unsecured debts, but some debts usually survive, such as most student loans, recent income taxes, child support, alimony, many court fines, and debts from fraud. Results depend on the chapter and your case.

Do I need to give CleanSlate Match my Social Security number or bank info?

No. We only collect contact details and general intent so we can connect you with a licensed bankruptcy attorney. Please do not send financial account numbers or other sensitive account details.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →