Guides

How much does bankruptcy cost?

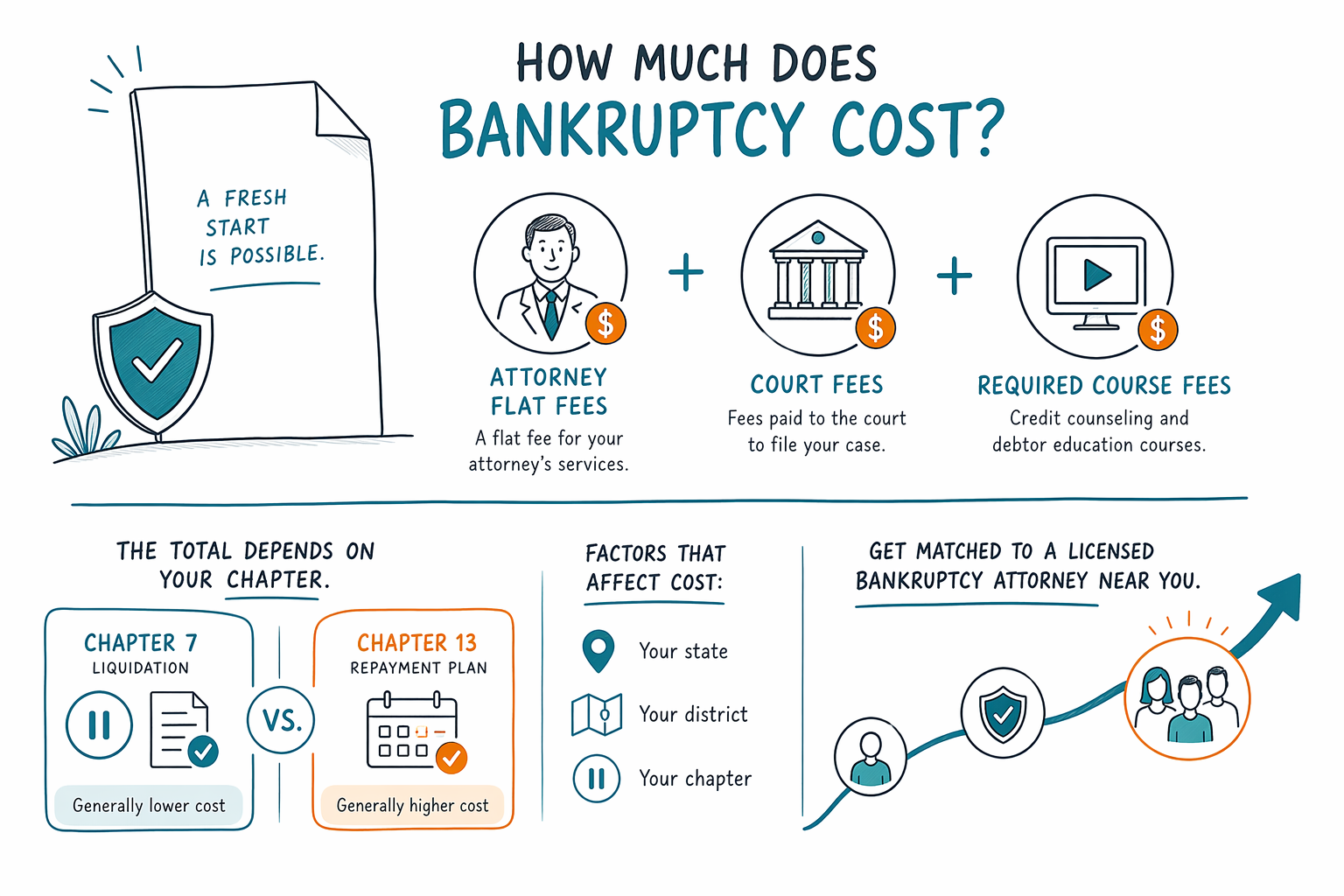

Bankruptcy has real costs, but you usually don’t pay a percentage of your debt. The exact price depends on where you live, which chapter fits your situation, and how complex your case is.

Quick answer: what most people pay (typical ranges)

Most consumer bankruptcy attorneys charge a flat fee for basic Chapter 7 or Chapter 13 work, plus you also pay the court filing fee and a small required credit-counseling fee.

Because bankruptcy rules and court costs vary by district and state, there isn’t one single number that fits everyone. A licensed attorney can give you the best estimate after reviewing your situation.

In many parts of the U.S., a common all-in range people discuss is roughly $2,000–$5,000+ for attorney fees plus court-related fees—though the final amount can be higher for more complex cases.

If you’re behind on payments, some attorneys may allow payment plans for their fees. Confirm the payment terms up front so you feel secure and not surprised.

What the costs usually include

Here are the parts that most people budget for:

1. Attorney’s flat fee (the lawyer’s work—review, forms, required filings, and representation through the key stages of your case).

2. Court filing fee (paid to the bankruptcy court). This fee amount can vary depending on the chapter and local procedures.

3. Required pre-filing credit counseling and related course fees (this is generally required before you file).

Depending on your situation, you might also have additional, case-specific costs (for example, if you need extra documentation or an interpreter-assisted process).

Chapter 7 vs. Chapter 13: why the price can differ

Bankruptcy cost often depends on whether you file Chapter 7 or Chapter 13.

- Chapter 7 is usually faster, and many attorneys price it with a relatively straightforward flat fee.

- Chapter 13 involves a repayment plan and ongoing filings, so it can take more attorney time. That’s one reason Chapter 13 is often priced higher than Chapter 7.

Also, the means test (the income-based eligibility step) and whether you have additional issues can affect complexity. Bankruptcy is not “one-size-fits-all,” and costs can change when a case has complications.

What makes the cost go up (and what can keep it down)

Costs vary by case. Common factors that can increase the price include:

- More complicated paperwork (multiple properties, several creditors, or unusual debts)

- Prior filings or prior bankruptcies

- Disputes about assets, titles, liens, or exemptions

- Wage garnishment, foreclosure, or active lawsuits that require extra preparation

Costs can be lower when the situation is simpler—fewer assets, straightforward debts, and clear documentation.

Important: any range is still just a guide. A licensed attorney in your area should confirm what applies in your district, after discussing your facts.

What bankruptcy costs cannot do: limits and “what survives”

It’s also fair to talk about limits. Bankruptcy is not a guaranteed “wipe out everything” button.

Some debts often survive bankruptcy, depending on the chapter and the details of your case—commonly including:

- Most student loans (usually very hard to discharge)

- Recent income taxes that don’t qualify under the rules

- Child support and alimony

- Court fines/penalties in many situations

- Debts involving certain kinds of misconduct (for example, fraud-related debts)

Outcomes depend on the individual case. A bankruptcy attorney can explain which debts are more likely to be discharged and which may not be.

Before you decide: get matched to a licensed attorney (free to you)

If you’re weighing bankruptcy, the best next step is to speak with a licensed bankruptcy attorney near you who can explain costs, eligibility, and what—if anything—can be discharged.

CleanSlate Match is a FREE matching service. We connect you with a participating, licensed bankruptcy attorney near you, but we are not a law firm and we don’t file bankruptcy. The attorney gives legal advice and confirms your options.

Rules vary by state and judicial district, and they can change. To avoid surprises, confirm the attorney’s flat fee, the court filing fee you’ll pay, and any required courses—plus whether the attorney offers payment plans.

If you want to start, visit get matched. For background on how bankruptcy chapters work, see chapters overview and guides.

Bankruptcy usually costs attorney flat fees plus court and required course fees, and the exact total depends on your state, district, and chapter—get matched to a licensed bankruptcy attorney near you to confirm what it will be for your case.

Common questions

Is bankruptcy free if I qualify?

There usually is no such thing as “free” bankruptcy. Most people pay attorney fees (often a flat fee) plus required court and course fees. A licensed attorney can estimate your likely total after learning the basics of your situation.

Will an attorney ask me for my bank account or Social Security number?

For CleanSlate Match, we collect contact information and a general sense of your situation and preferred language only—we don’t ask for Social Security numbers or bank-account details. Any legal screening questions should be limited to what the attorney needs, and you can ask what information is required.

Can bankruptcy stop a garnishment or foreclosure right away?

Often, the moment a bankruptcy case is filed, an automatic stay can pause many collections, including wage garnishment, foreclosure actions, and most lawsuits. The details depend on your case and timing, so confirm with a licensed bankruptcy attorney in your area.

How do I confirm I’m hiring a licensed attorney?

You can confirm an attorney’s license through your state’s bar or licensing authority. When matched, ask about the attorney’s experience with consumer bankruptcy and request a clear explanation of the flat fee and what it covers.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →