Guides

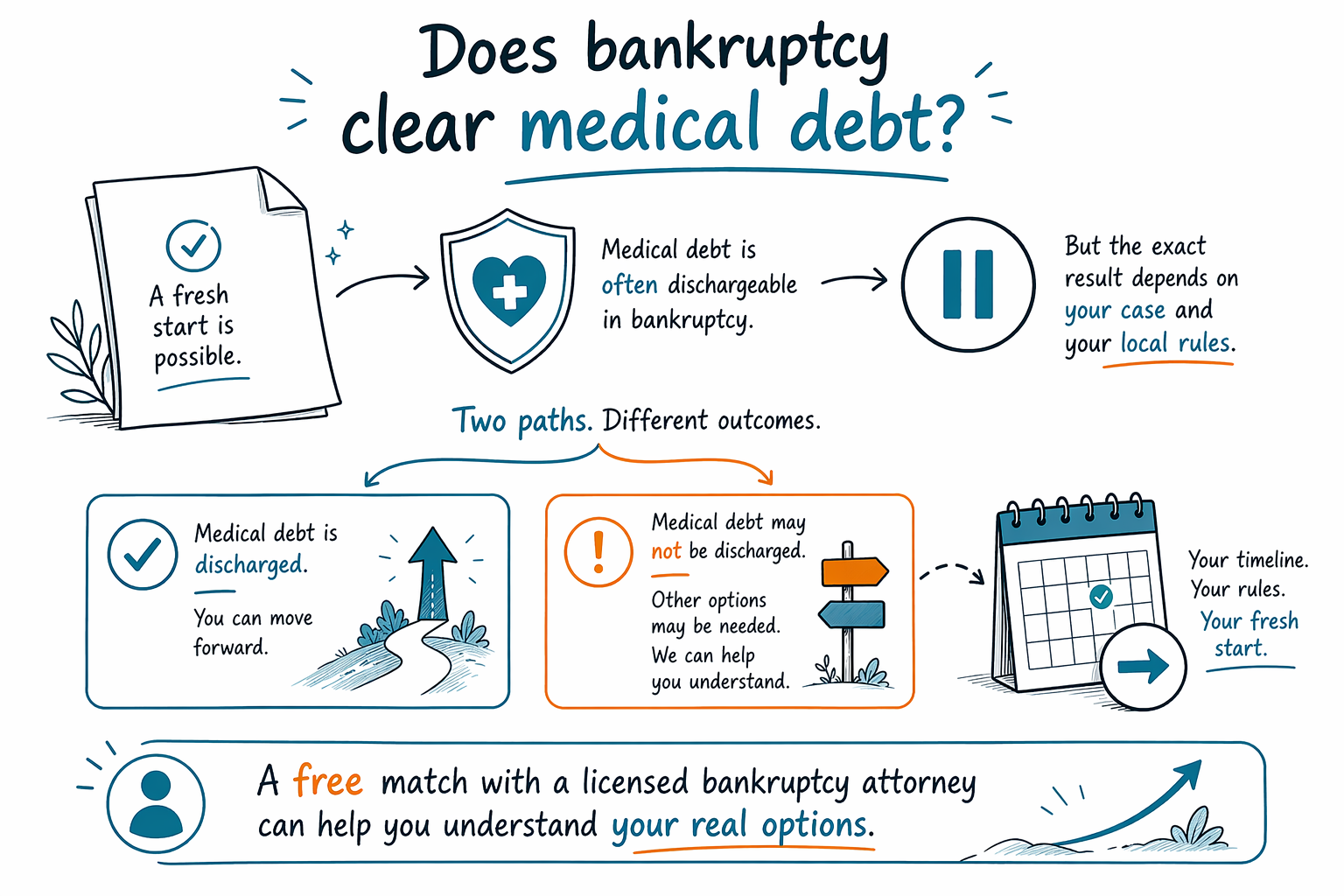

Does bankruptcy clear medical debt?

Yes, medical debt can often be discharged in bankruptcy, but not every case is the same. The rules vary by state and district, and a licensed bankruptcy attorney can help you understand what may happen in your situation.

Short answer: often yes, but not always

Medical bills are usually treated like unsecured debt, which means they are often dischargeable in Chapter 7 and may be paid, reduced, or discharged in Chapter 13 depending on the plan.

That said, bankruptcy does not erase everything. Some debts usually survive, including most student loans, recent income taxes, child support, alimony, many court fines, and debts tied to fraud.

The exact result depends on your facts, the chapter you file, and the rules in your state and federal district. A licensed bankruptcy attorney in your area can tell you what the law likely means for your case.

How medical debt is handled in Chapter 7 and Chapter 13

In Chapter 7, many people use bankruptcy to eliminate qualifying unsecured debts, including hospital bills, doctor bills, emergency room bills, and collection balances from medical providers or medical credit accounts.

In Chapter 13, you make a court-approved payment plan over time. Medical debt may be included with other unsecured debts and, in many cases, some or all of what is left after the plan can be discharged at the end.

Which chapter makes sense depends on your income, assets, whether you are behind on a house or car payment, and whether you are facing garnishment, lawsuits, or foreclosure. You can learn the basics in our Chapter 7 and Chapter 13 guides.

What bankruptcy can do right away

One important benefit is the automatic stay. When a bankruptcy case is filed, the automatic stay usually pauses most collection calls, letters, lawsuits, garnishments, and many other collection steps right away.

If your medical debt has been sent to collections, bankruptcy may also stop many collection actions while the case is moving through court. But not every situation is the same, and some actions can continue in limited circumstances.

If you are dealing with more than medical bills, the same protections may help with credit cards, personal loans, and other unsecured debts too. If you want a general overview first, start with our bankruptcy guides.

What bankruptcy usually does not clear

Bankruptcy can help with a lot of medical debt, but it is not a magic reset for every obligation. Some debts often remain even after bankruptcy, and some medical-related debts may need a closer review.

For example, if a bill is tied to fraud, a lawsuit judgment, or another special issue, the outcome can be different. Also, if a creditor claims a debt is not dischargeable, an attorney may need to review that claim.

This is one reason it helps to speak with a licensed bankruptcy attorney near you, rather than guessing from a form or a short online answer.

What CleanSlate Match does and what to expect

CleanSlate Match is a FREE matching service. We are not a law firm, not a lawyer, and we do not file bankruptcy or create an attorney-client relationship.

We collect only basic contact and general intent information, such as your name, phone number, optional email, state, preferred language, and a general description of your situation. We do not ask for Social Security numbers, bank account numbers, credit card numbers, or account balances.

If you choose to get matched, we can connect you with a licensed bankruptcy attorney near you so you can ask about your medical debt, your options, and whether Chapter 7 or Chapter 13 may fit your situation. You can begin here: get matched.

Medical debt is often dischargeable in bankruptcy, but the exact result depends on your case and your local rules, so a free match with a licensed bankruptcy attorney can help you understand your real options.

Common questions

Will medical debt disappear as soon as I file bankruptcy?

Filing bankruptcy usually triggers the automatic stay, which can pause most collection activity, but the final treatment of the debt depends on the chapter, the facts of your case, and the court rules. A licensed bankruptcy attorney can explain what happens in your district.

Can bankruptcy help if the hospital already sent my bill to collections?

Yes, often it can. Medical debt in collections is still commonly treated as unsecured debt, but you should have a local attorney review the account and any lawsuit papers, because details can matter.

How much does it cost to file bankruptcy for medical debt?

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The total depends on the chapter, the complexity of your case, and your district, so any range is only an estimate and not a quote.

Do I need to give CleanSlate Match my bank or account details?

No. We only collect contact information and a general sense of your situation, along with your state and preferred language. A lawyer may later ask for more details, but the matching service does not collect financial account numbers.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →