Guides

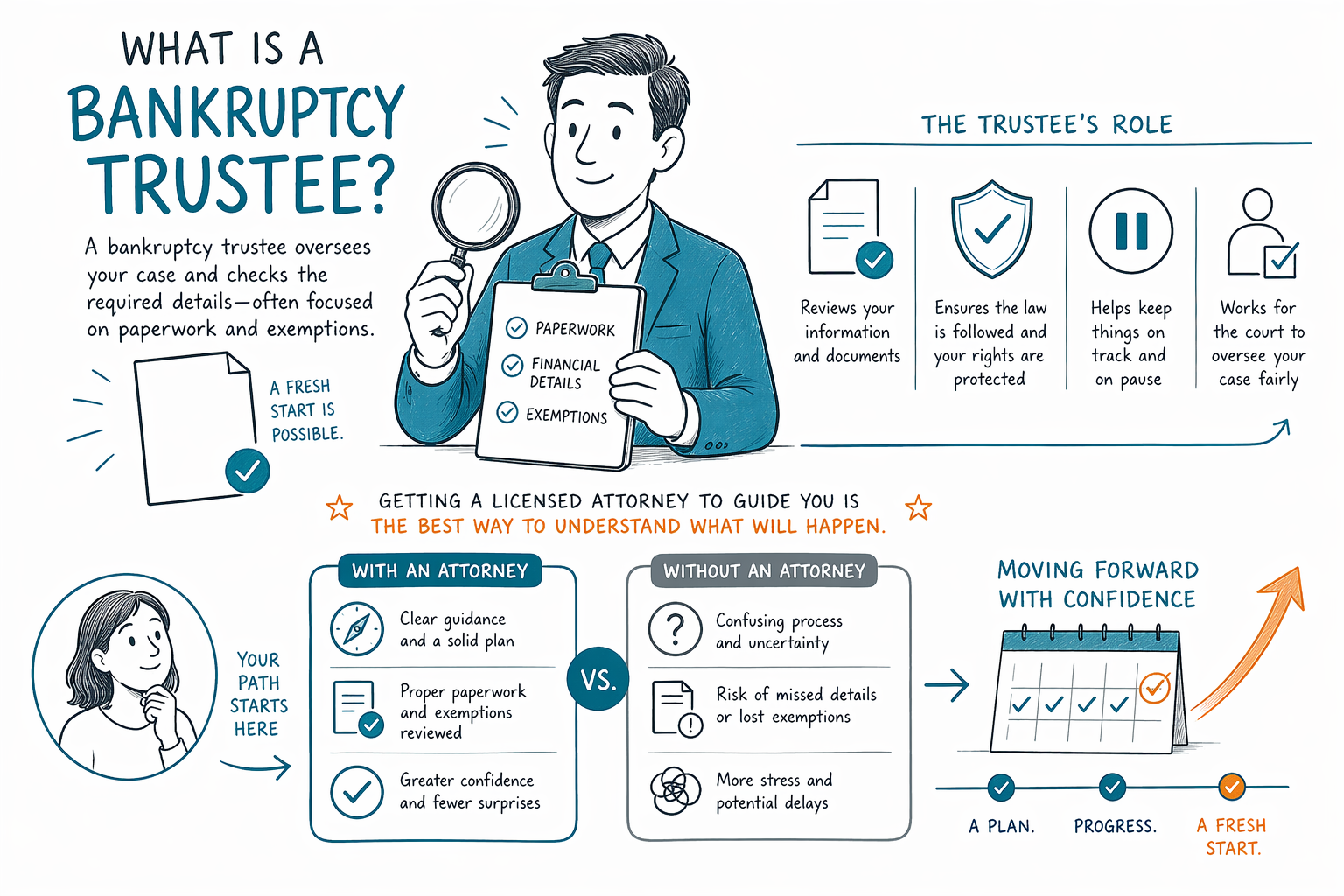

What is a bankruptcy trustee?

A bankruptcy trustee is a neutral person the court appoints to oversee your case and make sure the process follows the rules. Here’s what they do, what they can look at, and what to expect—so you feel less in the dark.

The direct answer: what a bankruptcy trustee does

In most consumer bankruptcy cases, a trustee is appointed by the court to review certain parts of your filing and help administer the case. Their job is to protect the integrity of the bankruptcy process and follow bankruptcy rules.

What a trustee focuses on depends on your situation and the chapter you file (Chapter 7 or Chapter 13). Often, many people never hand over personal paperwork directly to the trustee beyond what’s required in the case.

- You are not “being judged” by a trustee—they’re following a legal process.

- Your attorney handles most filings and communications with the court.

Chapter 7 trustee vs. Chapter 13 trustee (what changes)

In Chapter 7, the trustee may review whether you qualify for Chapter 7 under the means test and whether any non-exempt assets should be turned over for the benefit of creditors. If you have mostly exempt property, the trustee’s role may be limited.

In Chapter 13, the trustee is more involved in your repayment plan. Instead of creditors collecting directly, the trustee typically receives your plan payments and helps distribute them according to the court-approved plan and the law.

- Chapter 7: focus can include reviewing assets and the case paperwork.

- Chapter 13: focus can include administering plan payments.

What happens during the meeting with the trustee (and what to expect)

Many cases include a “341 meeting” (named for the section of the bankruptcy code). This is usually a meeting where the trustee can ask questions under oath about your debts, income, and what you listed in your paperwork.

This meeting is not the same as a courtroom trial. You typically answer questions from the trustee, and your bankruptcy attorney usually prepares you for what is commonly asked. If you feel overwhelmed, that’s a strong sign you’ll benefit from a licensed attorney guiding you step by step.

- Bring only what your attorney tells you to bring (usually identification and required documents).

- Be honest and consistent with your paperwork—your lawyer can help you clarify details.

Can a trustee take your stuff? Exemptions matter

Sometimes people worry the trustee will automatically take property. Usually, the key issue is whether the property is protected by bankruptcy exemptions.

Exemptions vary by state and sometimes by the specific district’s rules. A licensed bankruptcy attorney in your area can explain which exemptions are available to you and how they apply. Outcomes depend on your exact facts—there is no one-size-fits-all answer.

- Many people keep a home and/or car when they’re protected by exemptions or a Chapter 13 plan.

- Non-exempt assets may be reviewed for possible sale or distribution in some cases.

Limits: bankruptcy doesn’t erase everything

It’s important to know that some types of debt usually survive bankruptcy. Common examples include most student loans (especially unless a very specific hardship standard is met), recent income taxes, child support and alimony, many court fines, and debts connected to fraud or certain misconduct.

Also, the trustee’s involvement doesn’t change whether a particular debt can be erased—it’s the bankruptcy rules for your case. Because the rules vary by state and district and can change over time, confirm details with a licensed bankruptcy attorney near you.

- Some debts typically remain after bankruptcy.

- Your attorney can explain what usually happens to your specific debts.

How the trustee fits into the bigger picture—and how to get help fast

A trustee is one part of the court process. If you file, the bankruptcy “automatic stay” generally pauses many collections, garnishments, foreclosures, and lawsuits while the case is pending—so you can often stop the bleeding while you get your plan in order.

If you’re overwhelmed, CleanSlate Match can help you get connected with a licensed bankruptcy attorney near you for a consultation. CleanSlate Match is a FREE matching service (not a law firm and not your lawyer), and we only collect contact information and general intent—not SSNs or account details.

- Learn more about bankruptcy options: [Chapters overview](/chapters/).

- Start here: [Get matched](/get-matched/).

A bankruptcy trustee oversees your case and checks the required details—often focused on paperwork and exemptions—so getting a licensed attorney to guide you is the best way to understand what will happen in your district.

Common questions

Do I have to meet the trustee in person?

Often, yes—there is commonly a meeting (the 341 meeting) where the trustee asks questions. Whether it’s in person or by other means can vary by court and current procedures, so your attorney can confirm what to expect in your district.

Will the trustee contact me directly?

Usually, your bankruptcy attorney communicates with the trustee and the court as part of the process. You may still be asked questions during the meeting and may need to respond to specific requests, but you should not have to handle everything alone.

If the trustee is involved, does that mean I’ll lose everything?

Not necessarily. Many people keep property protected by exemptions. What happens depends on your state and district exemptions, what assets you own, and which chapter you file. A licensed bankruptcy attorney can explain your likely outcome based on your facts.

Can a trustee erase my debts?

The trustee does not “erase” debts. Bankruptcy discharge decisions depend on the bankruptcy chapter and the rules for your case. Some debts typically don’t discharge, and exceptions can apply.

Are bankruptcy trustee rules the same everywhere in the US?

No. While the trustee role is generally similar, procedures and exemption rules can vary by state and by the federal judicial district. It’s important to confirm details with a licensed bankruptcy attorney in your area.

How much does it cost to work with a bankruptcy attorney to deal with a trustee?

Fees vary, but many consumer bankruptcy attorneys charge a flat fee plus the required court filing fee and a small credit-counseling fee. The exact range depends on the chapter (Chapter 7 vs. Chapter 13), case complexity, and the district—ranges are not guaranteed quotes. Your attorney can review costs during the consultation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →