Guides

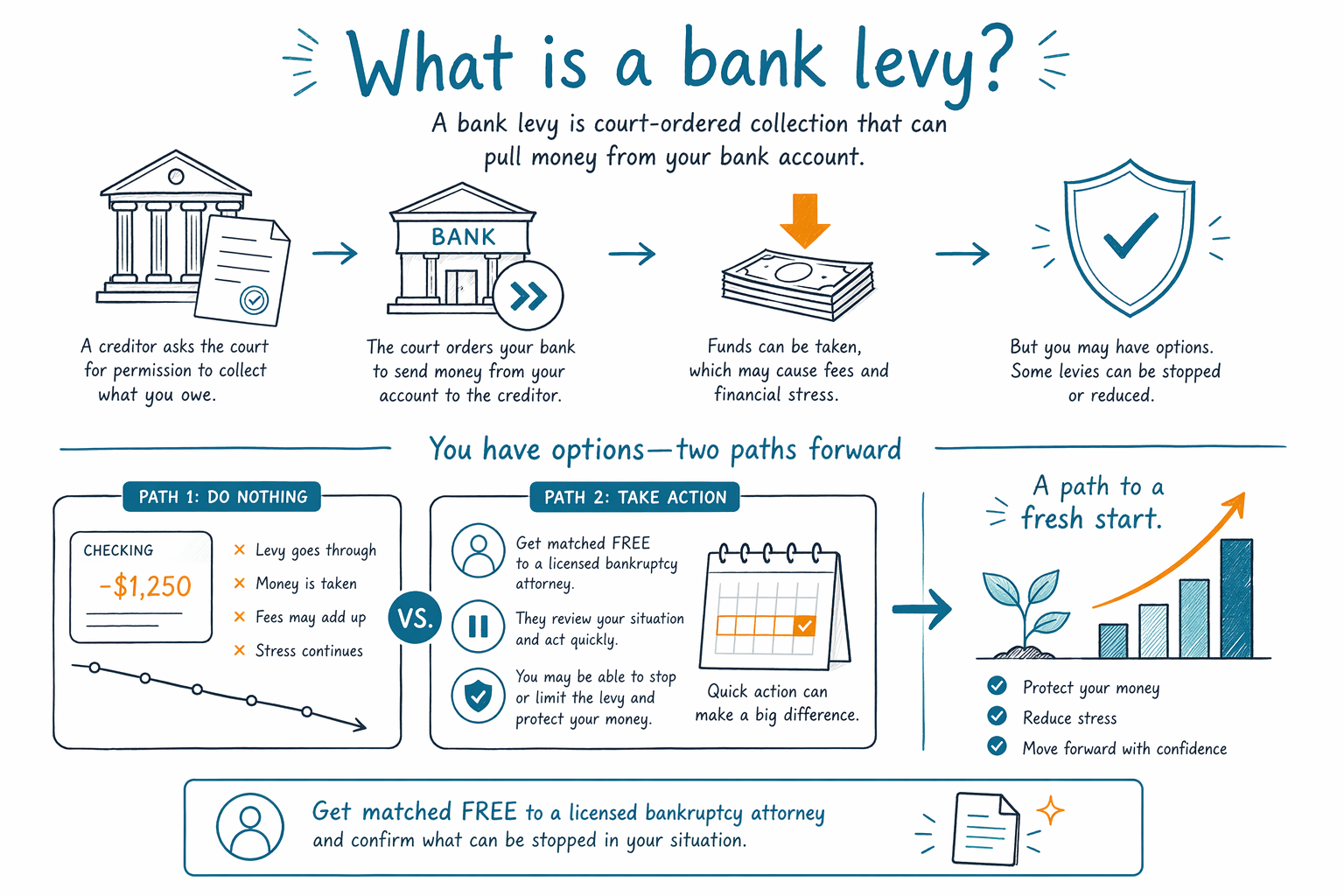

What is a bank levy?

A bank levy is when someone with a court order takes money directly from your bank account to help pay a debt. If this is happening to you, you may have options—start by learning what a levy means and get matched to a licensed attorney for help.

What a bank levy is (in plain terms)

A bank levy means a creditor (or a company collecting for them) uses a legal process to freeze and/or take funds from your bank account.

Often, the steps look like this: you get served with a court case or paperwork, the court enters a judgment (in many situations), and then a levy order is sent to your bank. When the order is received, the bank may hold the money and then release it to the creditor.

A bank levy can feel sudden and scary, but you’re not powerless. The right next steps depend on your situation and the type of debt.

- A levy is different from “you chose to pay” — it’s court-driven collection action

- Money can be frozen first, then released to the creditor depending on the order

How a levy usually affects your money

When your bank receives a levy order, they may freeze funds in the account up to the amount the creditor is seeking. Depending on state rules and the order, some money may be protected or exempt, but the creditor may still try to collect.

You might see your balance drop or transactions get declined. Even if the levy isn’t the full amount you owe, it can disrupt rent, groceries, transportation, or medicine.

If you’re facing a levy, try to act quickly. Missing a deadline or ignoring court papers can make things harder.

- Levy orders can disrupt day-to-day spending immediately

- Exemptions may exist, but they are not automatic—an attorney can explain what may apply

Do bank levies connect to wage garnishment or lawsuits?

Bank levies are part of the same general picture as other collection tools—like wage garnishment and some lawsuit-related enforcement. They typically come after a creditor has obtained the right to collect through the legal system.

If you also have a wage garnishment, a lawsuit, or foreclosure activity, it can feel like everything is happening at once. In many cases, people are dealing with multiple deadlines and different court processes.

A licensed bankruptcy attorney can help you understand how these actions interact in your district and what options may stop or slow them.

- A bank levy usually happens after a creditor reaches the enforcement stage

- Multiple collection actions can overlap, so timing matters

Can bankruptcy stop a bank levy?

In many consumer bankruptcy cases, filing can trigger an automatic stay. The automatic stay is a legal protection that generally pauses most collection actions—such as levies, garnishments, and foreclosure activity—once the case is filed.

That doesn’t mean every situation is identical. Some actions may be more complicated (for example, if a case was filed and dismissed before, or for certain types of debts). Outcomes also depend on the chapter you choose.

To understand how this would apply to you, review the basics of Chapter 7 vs. Chapter 13 and then speak with a licensed bankruptcy attorney in your area.

- The automatic stay can pause many collections after filing

- Rules and results depend on your case and local court rules

What bankruptcy usually can and cannot erase

Bankruptcy can often provide relief from many types of consumer debt, but it doesn’t erase everything in every case. Some debts usually survive bankruptcy.

Debts that commonly survive (not a complete list) include: most student loans, recent income taxes, child support/alimony, many court fines/penalties, and debts from fraud or certain misconduct. Also, whether you can keep certain property depends on exemptions that vary by state.

Because the details matter, confirm your options with a licensed bankruptcy attorney. Get matched with one near you—this matching service is free, but the attorney’s advice is what determines your best path.

- Some debts commonly survive bankruptcy—ask about yours specifically

- Exemptions and rules vary by state and judicial district

What to do right now if your bank account is being levied

If you think you’re facing a levy, the fastest way to protect yourself is to gather your court paperwork and contact a licensed bankruptcy attorney as soon as possible. Avoid stopping everything and waiting—deadlines can affect what options are available.

Here are practical steps that are generally helpful before you meet an attorney:

- Save the notices you received from the court, the creditor, or your bank

- Write down what actions you’ve been told about (levy, garnishment, lawsuit date, hearing date)

- Confirm your state of residence and the court location listed on the paperwork

- Prepare to ask your attorney what exemptions may apply to bank funds in your state

Remember: CleanSlate Match is a FREE matching service. We do not file bankruptcy, and we are not your lawyer. A licensed attorney can review your documents and explain your options honestly.

- Act quickly—paperwork and deadlines matter

- Don’t send sensitive banking details to a matching service

A bank levy is court-ordered collection that can pull money from your bank account, but you may have options—get matched free to a licensed bankruptcy attorney and confirm what can be stopped in your specific case.

Common questions

Is a bank levy the same as a “bank account freeze”?

They are related. A levy often leads to a freeze/hold of your account funds and then collection of money toward the debt, depending on the court order and timing.

Can I get my money back if my bank levy already happened?

Sometimes. It depends on whether exemptions applied, how the order was handled, and what steps were taken or missed. A bankruptcy attorney can explain possible options after reviewing your paperwork.

Will filing bankruptcy automatically stop everything, including a bank levy?

Often, filing triggers an automatic stay that pauses many collections after the case is filed. However, not every situation is the same, and results depend on your chapter, prior filings, the type of debt, and local rules.

How much does a bankruptcy attorney cost if I’m dealing with a levy?

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The total cost can vary by chapter (Chapter 7 vs. Chapter 13), case complexity, and the district—so ranges are best, and an attorney can confirm the numbers for your specific situation.

Does bankruptcy erase my debt that led to the levy?

Not always. Bankruptcy can discharge many debts, but some commonly survive—like many student loans, recent income taxes, child support/alimony, many fines/penalties, and debts tied to fraud or certain misconduct. The only honest way to know is to review your case with a licensed attorney.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →